How To Use A Mortgage Calculator

Mortgage Calculator

Use SmartAsset's mortgage calculator above to estimate your monthly mortgage payment, including your loan's principal, interest, taxes, homeowners insurance and individual mortgage insurance (PMI). You lot tin can adjust the home cost, down payment and mortgage terms to come across how your monthly payment volition change.

You can likewise attempt our how much house I can afford calculator if you're not sure how much coin you should upkeep for a new home.

A financial advisor can assist y'all in planning for the purchase of a home. To find a financial advisor who serves your surface area, try our costless online matching tool.

The Math Behind Our Mortgage Figurer

For those who want to know exactly how our reckoner works, we use the post-obit formula for our mortgage calculations:

M = Monthly Payment

P = Chief Amount (initial loan balance)

i = Interest Rate

n = Number of Monthly Payments for xxx-Year Mortgage (30 * 12 = 360, etc.)

How to Use Our Mortgage Payment Reckoner

The outset stride to determining what you'll pay each calendar month is providing groundwork data about your prospective home and mortgage. There are three fields to fill in: domicile cost, downward payment and mortgage interest rate. In the dropdown box, choose your loan term. Don't worry if you don't have exact numbers to work with - use your best approximate. The numbers tin ever exist adjusted later.

For a more detailed monthly payment calculation, click the dropdown for "Taxes, Insurance & HOA Fees." Here, y'all can fill up out the home location, annual property taxes, annual homeowners insurance and monthly HOA or condo fees, if applicable.

Dwelling Cost

Let's break it down farther. Dwelling house price, the start input, is based on your income, monthly debt payment, credit score and downwardly payment savings. A percentage you may hear when buying a dwelling house is the 36% rule. The dominion states that you should aim to for a debt-to-income (DTI) ratio of roughly 36% or less (or 43% maximum for a FHA loan) when applying for a mortgage loan. This ratio helps your lender empathize your financial capacity to pay your mortgage each month. The higher the ratio, the less likely it is that you can beget the mortgage.

To calculate your DTI, add all your monthly debt payments, such every bit credit card debt, pupil loans, alimony or kid support, auto loans and projected mortgage payments. Next, split up by your monthly, pre-revenue enhancement income. To become a percentage, multiple by 100. The number you're left with is your DTI.

DTI = Full Monthly Debt Payments ÷ Gross Monthly Income 10 100

Downwardly Payment

In full general, a 20% downwards payment is what virtually mortgage lenders await for a conventional loan with no individual mortgage insurance (PMI). Of course, there are exceptions. For example, VA loans don't require down payments and FHA loans ofttimes permit as depression equally a 3% down payment (merely do come with a version of mortgage insurance). Additionally, some lenders have programs offer mortgages with down payments as depression every bit iii% to 5%. The table below shows how the size of your down payment will bear on your monthly mortgage payment.

*The payment is main and involvement only. To go the total monthly payment for down payments below 20%, add in your property taxes, homeowners insurance and individual mortgage insurance (PMI).

In full general, near homebuyers should aim to have 20% of their desired habitation price saved before applying for a mortgage. Being able to make a sizeable downwardly payment improves your chances of qualifying for the best mortgage rates. Your credit score and income are two additional factors that play a role in determining your mortgage charge per unit and, therefore, your payments over time.

Mortgage Rate

For the mortgage charge per unit box, you can encounter what yous'd authorize for with our mortgage rates comparison tool. Or, you can use the interest rate a potential lender gave you when y'all went through the preapproval process or spoke with a mortgage banker. If you don't have an idea of what you'd qualify for, you can always put an estimated charge per unit past using the current charge per unit trends found on our site or on your lender's mortgage page. Remember, your actual mortgage rate is based on a number of factors, including your credit score and debt-to-income ratio.

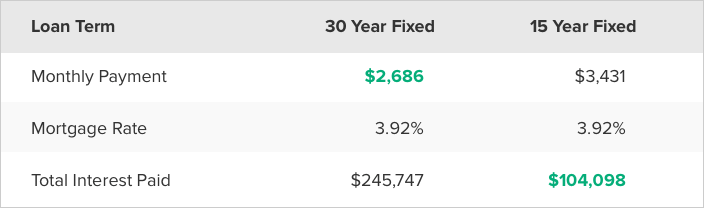

Loan Term

In the drop down surface area, yous have the choice of selecting a 30-year fixed-charge per unit mortgage, 15-year fixed-rate mortgage or v/ane ARM. The kickoff two options, as their proper name indicates, are stock-still-rate loans. This means your involvement rate and monthly payments stay the same over the form of the entire loan. An ARM, or adjustable rate mortgage, has an interest rate that volition alter after an initial stock-still-rate catamenia. In general, following the introductory menses, an ARM's interest rate will change once a year. Depending on the economic climate, your rate can increment or decrease. Well-nigh people choose 30-year fixed-rate loans, but if you're planning on moving in a few years or flipping the house, an ARM can potentially offer you a lower initial rate.

Understanding Your Mortgage Payment

Monthly mortgage payment = Principal + Interest + Escrow Account Payment

Escrow business relationship = Homeowners Insurance + Holding Taxes + PMI (if applicable)

The lump sum due each month to your mortgage lender breaks down into several different items. Almost homebuyers have an escrow account, which is the business relationship your lender uses to pay your property tax beak and homeowners insurance. That means the bill you receive each month for your mortgage includes not just the principal and interest payment (the money that goes directly toward your loan), just too property taxes, home insurance and, in some cases, private mortgage insurance.

What Is Master and Interest?

The master is the loan amount that you borrowed and the involvement is the additional coin that yous owe to the lender that accrues over fourth dimension and is a pct of your initial loan. Fixed-rate mortgages will have the same full primary and involvement amount each month, but the actual numbers for each modify equally you pay off the loan. This is known as amortization. You start by paying a higher percentage of involvement than principal. Gradually, you'll pay more than and more principal and less interest. Run across the table below for an instance of acquittal on a $200,000 mortgage.

*This table depicts loan amortization for a $200,000 fixed-rate, xxx-year mortgage.

What Is Homeowners Insurance?

Homeowners insurance is a policy you purchase from an insurance provider that covers you in case of theft, burn down or storm damage (hail, wind and lightning) to your home. Inundation or earthquake insurance is generally a carve up policy. Homeowners insurance can cost anywhere from a few hundred dollars to thousands of dollars depending on the size and location of the dwelling house.

When you infringe money to buy a domicile, your lender requires you lot to have homeowners insurance. This blazon of insurance policy protects the lender's collateral (your home) in case of fire or other damage-causing events.

How Do Belongings Taxes Piece of work?

When you own property, you're subject to taxes levied by the canton and district. You can input your naught code or town name using our property tax calculator to see the average constructive revenue enhancement charge per unit in your area.

Property taxes vary widely from state to state and fifty-fifty county to county. For instance, New Bailiwick of jersey has the highest average effective property taxation charge per unit in the country at 2.42%. Owning belongings in Wyoming, however, will only put yous dorsum roughly 0.57% in holding taxes, one of the everyman boilerplate effective taxation rates in the country.

While it depends on your state, county and municipality, in full general, holding taxes are calculated as a percentage of your dwelling'southward value and billed to yous one time a year. In some areas, your abode is reassessed each year, while in others information technology can be as long as every five years. These taxes generally pay for services such equally road repairs and maintenance, school district budgets and county general services.

What Is PMI?

Private mortgage insurance (PMI) is an insurance policy required by lenders to secure a loan that's considered high risk. Y'all're required to pay PMI if yous don't take a 20% downwardly payment and you lot don't qualify for a VA loan. The reason most lenders require a 20% downward payment is due to equity. If y'all don't have loftier enough equity in the domicile, you're considered a possible default liability. In simpler terms, you represent more than run a risk to your lender when yous don't pay for plenty of the home.

PMI is calculated as a percent of your original loan amount and tin can range from 0.3% to 1.v% depending on your downward payment and credit score. Once you lot accomplish at least 20% equity, you can request to finish paying PMI.

What Are HOA Fees?

Homeowners association (HOA) fees are common when you buy a condominium or a home that'south function of a planned community. Generally, HOA fees are charged monthly or yearly. The fees comprehend mutual charges, such as community space upkeep (such equally the grass, community puddle or other shared amenities) and building maintenance. When y'all're looking at properties, HOA fees are normally disclosed upfront, then you can run into how much the current owners pay per month or per yr. HOA fees are an additional ongoing fee to debate with, they don't comprehend belongings taxes or homeowners insurance in nigh cases.

How to Lower Your Monthly Mortgage Payment

- Cull a long loan term

- Buy a less expensive house

- Pay a larger down payment

- Discover the lowest involvement charge per unit bachelor to you

Yous tin await a smaller bill if you increment the number of years y'all're paying the mortgage. That means extending the loan term. For example, a 15-year mortgage will have college monthly payments than a xxx-year mortgage loan, because you're paying the loan off in a compressed amount of time.

An obvious but nevertheless important road to a lower monthly payment is to buy a more affordable dwelling. The higher the home cost, the higher your monthly payments. This ties into PMI. If you lot don't accept plenty saved for a twenty% downward payment, you're going to pay more each month to secure the loan. Ownership a home for a lower toll or waiting until you lot take larger downwardly payment savings are two ways to save you from larger monthly payments.

Finally, your interest charge per unit impacts your monthly payments. You don't have to accept the first terms you become from a lender. Try shopping effectually with other lenders to find a lower rate and keep your monthly mortgage payments as low equally possible.

How To Use A Mortgage Calculator,

Source: https://smartasset.com/mortgage/mortgage-calculator

Posted by: gatewoodbeed1961.blogspot.com

0 Response to "How To Use A Mortgage Calculator"

Post a Comment